File GSTR 1 return by using offline excel tool. This

Read how to Install GSTR 1 offline tool on your computer. Similarly, learn how to prepare and file GSTR 1 in offline mode. GSTR 1 offline format will save your lot of time and internet usage than that actual online filing on GST portal. Thus GSTR 1 format in excel plays a very important role for filing return under Goods and service tax in India.

Download GSTR 1 Format in pdf

You may download GSTR 1 format in pdf format for offline use. This GSTR 1 form in pdf format is as per GST rules. Click on below link to download GSTR 1 in pdf format.

GSTR 1 Format Filing Instructions

Here are the GSTR 1 filing instructions as per CGST rules. However, the actual filing steps may vary for GSTR 1 offline filing and GSTR 1 online filing process. You will find GSTR 1 filing instructions in above GSTR 1 format in excel once you download it.

| Sr.no. | Details |

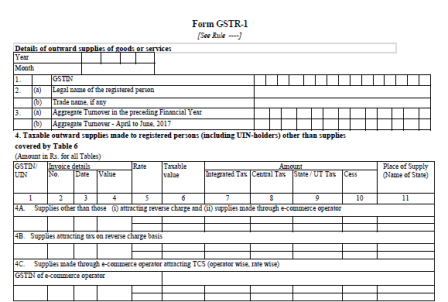

| 1. | Terms used: a. GSTIN: Goods and Services Tax Identification Number b. UIN: Unique Identity Number c. UQC: Unit Quantity Code d. HSN: Harmonized System of Nomenclature e. POS: Place of Supply (Respective State) f. B to B: From one registered person to another registered person g. B to C: From registered person to unregistered person |

| 2. | The details in GSTR 1 shall be furnished by 10thof the month succeeding the relevant tax period. Check GSTR 1 due date from here. |

| 3. | The Aggregate turnover of the taxpayer for the immediate, preceding financial year and first quarter of the current financial year shall be reported in the preliminary information in Table 3. This information would be required to be submitted by the taxpayers only in the first year. Quarterly turnover information shall not be captured in subsequent returns. Thus, Aggregate turnover shall be auto-populated in subsequent years. |

| 4. | Invoice-level information pertaining to the tax period should be reported for all supplies as under: (i) For all B to B supplies (whether inter-State or intra-State), invoice level details, rate-wise, should be uploaded in Table 4, including supplies attracting the reverse charge and those effected through e-commerce operator. Outwards supply information in these categories (ii) For all inter-State B to C supplies, where invoice value is more than Rs. 2,50,000/- (B to C Large) invoice level details, rate-wise, should be uploaded in Table 5; and (iii) For all B to C supplies (whether inter-State or intra-State) where invoice value is up to Rs. 2,50,000/ – State-wise summary of supplies, rate-wise, should be uploaded in Table 7. |

| 5. | Table 4 capturing information relating to B to B supplies should: (i) be captured in: a. Table 4A for supplies relating to other than reverse charge/ made through e-commerce operator, rate-wise; b. Table 4B for supplies attracting the reverse charge, rate-wise; and c. Table 4C relating to supplies effected through e-commerce operator attracting the operator wise and rate-wise. (ii) Capture Place of Supply (PoS) only if the same is different from the location of the recipient. |

| 6. | Table 5 to capture information of B to C Large invoices and other information shall be similar to Table 4. The Place of Supply (PoS) column is mandatory in this table. |

| 7. | Table 6 to capture information related to: (i) Exports out of India (ii) Supplies to SEZ unit/ and SEZ developer (iii) Deemed Exports |

| 8. | Table 6 needs to capture information about the shipping bill and its date. However, if the shipping bill details are not available, Table 6 will still accept the information. However, the same can be updated through the submission of information in relation to amendment Table 9 in the tax period in which the details are available but before claiming any refund/rebate related to the said invoice. Further, the detail of Shipping Bill shall be furnished in 13 digits capturing port code (six digits) followed by the |

| 9. | Any supply made by SEZ to DTA, without the cover of a bill of entry is required to be reported by the SEZ unit in GSTR -1. Also, the supplies made by SEZ on the cover of a bill of entry shall be reported by |

| 10. | In case of export transactions, GSTIN of the |

| 11. | Export transactions effected without payment of IGST (under Bond/ Letter of Undertaking (LUT)) needs to be reported under ―0‖ tax amount heading in Table 6A and 6B. |

| 12. | Table 7 to capture information in respect of the taxable supply of: (i)B to C supplies (whether inter-State or intra-State)with invoice value uptoRs 2,50,000; (ii)Taxable value net of debit/credit note raised in a particular tax period and information pertaining to previous tax periods which was not reported (iii)Transactions effected through e-commerce operator attracting the collection of tax at source under section 52 of the Act to be provided operator wise and rate wise; (iv)Table 7A (1) to capture gross intra-State supplies, rate-wise, including supplies made through e-commerce operator attracting the collection of tax at source and Table 7A (2) to capture supplies made through e-commerce operator attracting the collection of tax at source out of gross supplies reported in Table 7A (1); (v)Table 7B (1) to capture gross inter-State supplies including supplies made through e-commerce operator attracting the collection of tax at source and Table 7B (2) to capture supplies made through e-commerce operator attracting the collection of tax at source out of gross supplies reported in Table 7B (1); and (vi)Table 7B to capture information State wise and rate wise. |

| 13. | Table 9 to capture information of:(i)Amendments of B to B supplies reported in Table 4, B to C Large supplies reported in Table 5 and Supplies involving exports/ SEZ unit or SEZ developer/ deemed exports reported in Table 6; (ii)Information to be captured rate-wise; (iii)It also captures original information of debit/credit note issued (iv)Place of Supply (PoS) only if the same is different from the location of the recipient; (v)Any debit/ credit note pertaining to invoices issued before the appointed day under the existing law also to be reported in this table; and Shipping bill to be provided only in case of exports transactions amendment. |

| 14. | Table 10 is similar to Table 9 but captures amendment information related to B to C supplies and reported in Table 7. |

| 15. | Table 11A captures information related to advances received, rate-wise, in the tax period and tax to be paid thereon along with the respective PoS. It also includes information in Table 11B for adjustment of tax paid on advance received and reported in earlier tax periods against invoices issued in the current tax period. The details of information relating to advances would be submitted only if the invoice has not been issued in the same tax period in which the advance was received. |

| 16. | Summary of supplies effected against a particular HSN code to be reported only in summary table. It will be optional for taxpayers having annual turnover uptoRs. 1.50 Cr but they need to provide information about the |

| 17. | It will be mandatory to report HSN code at two digits level for taxpayers having the *Note: |

GSTR 1 JSON to Excel Converter

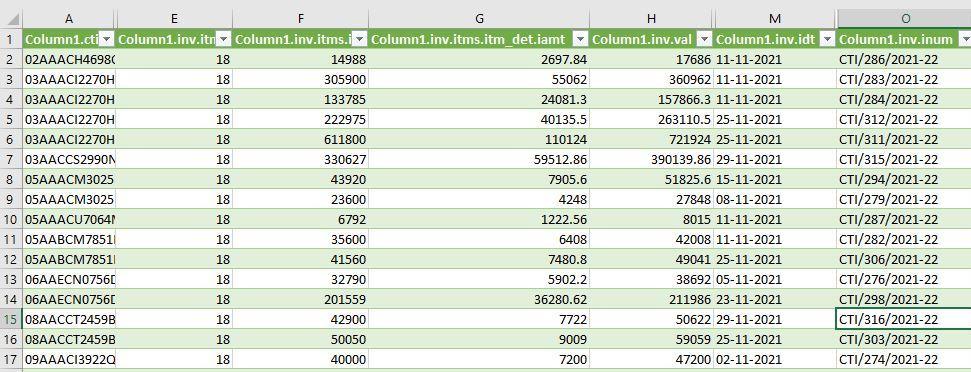

You may want to convert the downloaded GSTR 1 .json file from the GST portal into the excel sheet. There may be a number of online tools available which may convert your JSON file to excel. However, these may not give you the exact data the way you want. Also, sometimes you may not want to upload your JSON file on the third-party website containing the important data. You can extract the JSON file data as shown in the below image by using MS Excel.

Here we are going to discuss how you can import or convert your GSTR 1 JSON file into a Microsoft Excel file. Here is the step-by-step guide.

Time needed: 5 minutes

- Open the Microsoft Excel

- Click on the “Data” tab

- Click on “New Query”

(Do not click on Get External Data” option

- Select the option “From Web” or “From JSON or “From other sources >> From Web”

If you are using office 365, you will see the option from JSON. You can also open the “Launch power query editor”

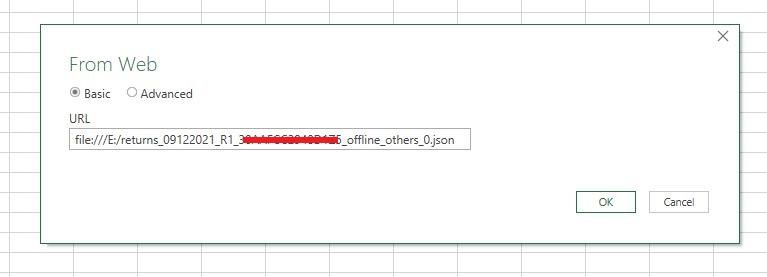

- Copy the JSON file link > OK

Copy the file path of the downloaded JSON file, from the GST portal. In the below path, I have saved my file in e: drive

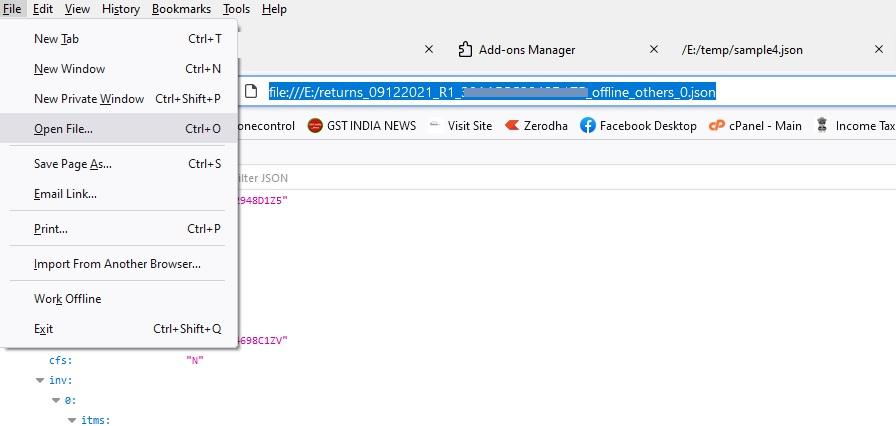

How to copy the path?

Open the JSON file in the browser >> Right-click on the path and click copy

- Paste the JSON file path into the excel file >> Press the Ok button

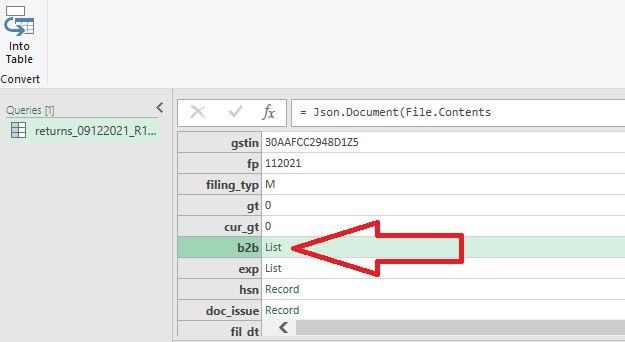

- Now click on on the list as shown below

This will get the b2b entries in the excel sheet. if you want b2c data you may click on b2c.

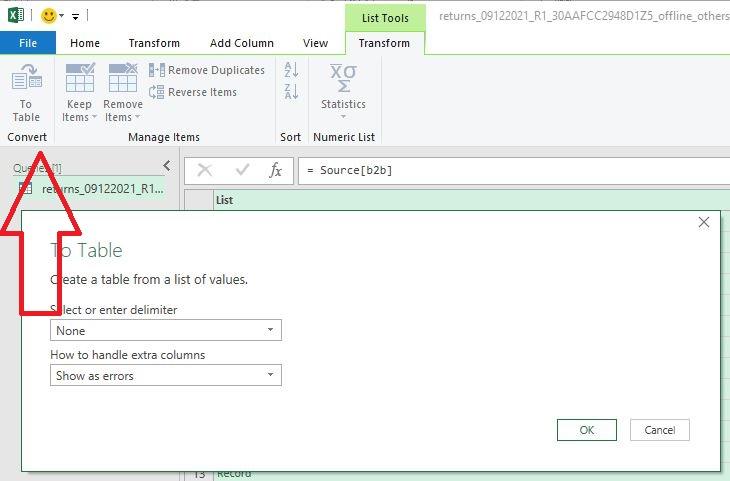

- Now click on “To table”. On the next window, click ok.

Clicking on this option will convert your data into the table format

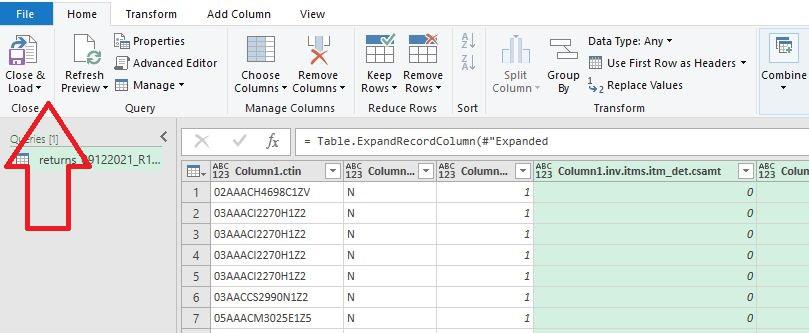

- Finally, click on the “Close and load” Option from the left-hand side.

This step will load the data in the excel file. The loaded data can now be used in many ways like vlookup, sort, pivot table, etc.

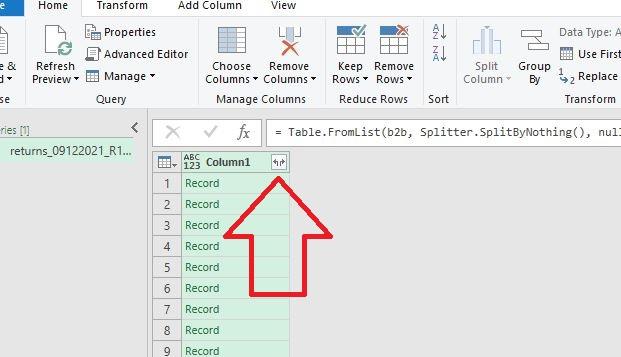

- Expand the data columns >> Expand new rows >> Ok.

In order to see the complete data click on the expand sign as shown below. you can keep on expanding the columns till you see the below sign so that the JSON file can fetch all the existing data in the JSON file of the selected sheet. No need to choose any options after clicking on the expand sign, simply hit ok.

By using the above steps you can easily convert not only GSTR 1 JSON file but any other GST-related JSON file in excel. Similarly, these steps are useful beyond the GST JSON file. Thus, the process can be used for another JSON file that contains this type of huge data.

FAQ on GSTR 1

Question 1: In which table Supplies to SEZ to be shown of GSTR 1 Return

Answer1: Supplies to SEZ should be shown in Table 6B of GSTR 1 Return.

Question 2: What happens where the details of inward supplies furnished by the recipient do not match with the outward supply details furnished by the supplier in his valid return?

Answer 2: In case of a mismatch, communication would be made to both parties. If the mismatch is not rectified, then the amount will be added to the output liability of the recipient in the return for the month succeeding the month in which the discrepancy is communicated.

Question 3: What is Table 6A of GSTR 1 Return?

Answer 3: Table 6A of GSTR 1 is meant for providing details of Export supplies made by the taxpayer during the given period. The taxpayer should furnish these details in Table 6A if he intends to claim a refund of ITC (Input Tax credit) of tax paid on Export supplies. These details of export invoices have been entered in this table.

Related: How to resolve https //127.0.0.1:1585 error?

Who should file Table 6A of form GSTR 1, and why?

Any Registered taxable person, other then Input Service Distributor (ISD), Compounding Tax payer, TDS Deductor, TCS Collector and who wants to claim Refund on taxes paid on Exports made should file Table 6A of Form GSTR 1 electronically on GST Portal.

General Questions

1. Go to GST portal

2. Click on Downloads >> Offline tools

3. Click on “Returns Offline Tool“

4. Click on Download

1. Unzip the downloaded file

2. Run the GST Offline Tool.exe from the extracted folder.

3. Complete the installation.

4. Open the GSTR1_Excel_Workbook_Template_V1.5.xlsx

5. Fill the data in above excel file.

1. Open the installed GST offline Tool (Icon on Desktop)

2. Import the excel data file in the above offline tool.

3. Generate the JSON file.

4. Login to GST portal.

5. Upload the JSON file by choosing “Prepare Offline” option.

1. Choose “Prepare Online” Option

2. Verify the details and click on submit.

3. Click on “File Return” to file the return.

How to show 6% IGST OR 3% CGST in GSTR 1?

A new concessional GST tax rate of 6% IGST or 3% CGST+ 3% SGST has been implemented for certain goods vide Notification No. 02/2022 dated 31st March 2022.

Thus, the changes are being made to the GST portal to include this rate in GSTR-1. Hence as a temporary measure, taxpayers who have to report goods at this rate may do so by reporting the entries in the 5% heading and then manually increasing the system computed tax amount to 6%.

The taxpayer can do this by entering the value in the ‘Taxable value’ column next to the 5% tax rate. Later the taxpayer has to increase the system computed tax-amount to 6% IGST or 3% CGST + 3% SGST in the ‘Amount of Tax’ column. This has to update under the relevant Table, namely B2B, B2C or Export, as applicable.

This process will ensure that the correct tax amount is reported in GSTR-1. The GSTN team will update this rate change provision shortly on the GST portal.

Read: How to File Returns under QRMP Scheme?

GSTR-1 return मे अगर किसी बिल की डिटेल गलत चली गयी है तो उसको कैसे CORRECTION होगा…

you can amend the details in the next month GSTR 1 by going through amendment tile or correct it by sending credit note/debit to the customer for tax/amount difference.

In gstr 1 return I found the below error. Plz help how it solve

“Based on your filing preference (quarterly), you are only allowed to import details for B2B, CDNR, B2BA and CDNRA tables for selected period. Please use the latest version of offline tool available on the GST portal to generate the JSON file.

This is a json structure error. you may find more information on this from here https://gstindianews.info/error-json-structure-validation-gst-solution/

Also, you may try downloading the latest offline tool to upload the invoices and check.

regards

HI,

I want to sell my goods to an unregistered dealer..

How do I show it in GSTR 1 return?

And what are the tax implications ?

How invoice should be prepared ?

Should I charge GST in invoice or not ?

please clarify..

hello Ashish

Follow these simple steps:

1 show the sales transactions under B2C block

2 prepare invoice similar to GST Registered person

4 charge GST In invoice

regards

jayendra

I want to maintain my sales in GSTR 1 excel format, but I do not know how to add invoice to the excel sheet that have multiple items with multiple tax rates. please help…

hello,

download the offline tool from the gst portal and you can add as many records..

regards

hi,

i want to download GSTR 1- details in excel to cross check with books, Please guide me

hello,

Now you can follow the above steps to convert gstr 1 to json.

regards

Hello sir,

1. Is Reverse Charge applicable for B2B. Because in GSTR 1 , Reverse Charge is asking for 4A,4B,4C ? If yes Please let me know the scenario.

2. Can be created E-invoice for Credit Note for registered Person?

hi

1. Please read it here about reverse charge on outward supplies >> https://gstindianews.info/reverse-charge-mechanism-in-gst-meaning. On outward

supplies if the tax is payable by the recipient, such supplies should be shown under b2b reverse charge column.

2. e-invoice needs to be generated for credit note and debit notes if issued under Section 34 of CGST/SGST act >> Refer sec. 34 https://gstindianews.info/cgst-section-29-40

I hope this helps

regards

I want to download GST R1, GST R3B, And B2B

But I don’t able to download please guide me